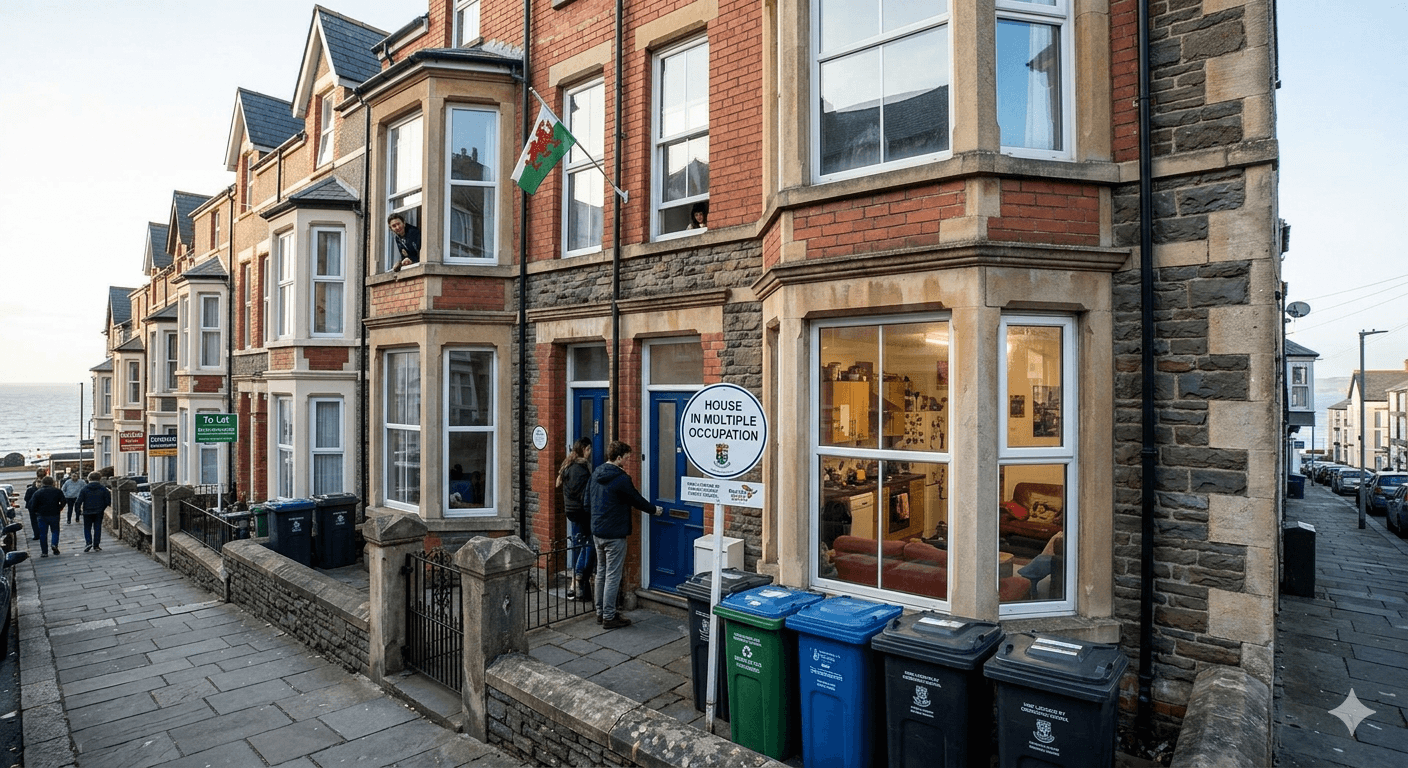

Single Council Tax Band for HMOs in Wales: What Landlords Need to Know in 2026

HMOs in Wales are moving to a single council tax band, with liability shifting to landlords. While this simplifies the system, the real impact lies in how it affects yields, risk, and deal structuring for investors.

Recent changes to council tax rules for Houses in Multiple Occupation (HMOs) in Wales are being widely discussed—but often misunderstood.

The headline is simple:

HMOs will generally be treated as a single dwelling, with council tax liability shifting to the landlord.

The reality is more nuanced—and for investors, the implications are significant.

What’s actually changing?

The Council Tax (Chargeable Dwellings and Liability for Owners) (Amendment) (Wales) Regulations 2026, laid before Senedd Cymru on 24 March 2026, aim to standardise how HMOs are treated for council tax.

Under the new framework:

Properties meeting the legal definition of an HMO under the Housing Act 2004 will generally be valued as a single dwelling

Council tax liability will sit with the property owner, not the tenants

The previous ability to disaggregate properties into multiple council tax bands (e.g. per room or unit) will largely be removed

The rules apply to both licensed and unlicensed HMOs

This brings consistency to a system that has historically varied depending on property configuration and local interpretation.

When do the changes take effect?

The regulations are expected to come into force during 2026, with industry guidance indicating implementation from around June 2026.

However, this should be treated as an indicative timeframe rather than a fixed date, as commencement depends on the legislative process.

The changes are not retrospective and will apply going forward.

Why this matters for HMO investors

Most commentary focuses on simplification. The more important point is how this affects returns and risk.

1. Council tax becomes a landlord cost

In many HMOs, council tax has historically been:

Paid directly by tenants

Or effectively passed through

Under the new rules, it becomes a direct operating expense.

This impacts:

Net yield

Cashflow modelling

Rent-setting strategy

2. Structural advantages are being removed

Previously, some landlords benefited from:

Multiple lower council tax bands

Creative layouts that reduced total liability

This reform removes much of that flexibility.

The result is:

A more level playing field

Fewer opportunities for structural optimisation

3. The impact varies by property

There is no universal outcome.

For example:

A 5-bed HMO previously split into Band A units may see higher overall council tax under a single band

A property already treated as one dwelling is likely to see minimal change

The key takeaway is that every deal needs to be reassessed individually.

Important nuance: not all properties are treated the same

The changes apply to HMOs as defined under the Housing Act 2004.

However:

Fully self-contained units (e.g. studios with their own kitchen and bathroom) may still be banded separately

Classification depends on the physical and legal structure of the property

Misunderstanding this can lead to incorrect assumptions and materially affect returns.

What landlords should do now

As the rules come into force, landlords should:

Review how their properties are currently banded

Reassess expected council tax liability

Factor this into yield and stress testing

Engage with the Valuation Office Agency if re-banding is required

In practice, implementation may involve a transition period as properties are reassessed.

Our view

At Jeric Properties, we see this as a move toward standardisation rather than restriction.

The opportunity in HMOs remains strong, but the source of returns is shifting.

Going forward:

Less reliance on structural quirks

Greater emphasis on acquisition discipline and operational efficiency

The easy wins are being removed. The fundamentals matter more.

Final thoughts

The 2026 council tax changes for HMOs in Wales are not a tax break or a new incentive.

They are a clarification of rules and a shift in liability.

For investors, the key is simple:

Understand the detail, not just the headline.

Small regulatory changes like this often have outsized effects on long-term performance.

Considering HMOs in Wales?

If you’re actively reviewing HMO opportunities, understanding how changes like this impact yield and structure is critical.

At Jeric Properties, we assess every deal based on income, structure, and long-term performance—not just headline pricing.

If you’re working on a deal or want a second opinion, feel free to reach out:

Email: hello@jericproperties.co.uk

WhatsApp: Message us directly

We’re happy to share how we’re approaching opportunities in the current market.